Last Updated on December 14, 2022

Getting a college education is an investment in your future. But paying for it isn’t always easy—especially considering the rising cost of tuition.

Luckily, there are a number of ways you can make that investment easier on your wallet. The most popular option is federal student loans, which come with several benefits that make them an attractive option for many students.

Here are some of the biggest benefits of federal student loans:

1) They’re flexible: Federal student loans allow you to choose how much money you’d like to borrow and set up payments that fit your budget. They also offer repayment plans with low fixed rates and no origination fees, so you can pay off your debt without worrying about interest charges or late penalties.

2) You don’t need good credit: Unlike many private lenders, the federal government doesn’t require a strong credit history in order to qualify for federal student loans—and even if you don’t have a good score yet (or any score at all), they may still be able to help you find funding for your education.

3) You’re not responsible for paying interest until after graduation: Federal loans don’t accrue interest while you’re in school; instead, it starts adding up as soon.

Who is eligible for federal loan consolidation?

To be eligible for Federal Loan Consolidation, borrowers must have at least one loan from the Federal Direct Loan program or Federal Family Education Loan (FFEL) program that is not in an “in-school” status.

Are defaulted borrowers eligible for federal loan consolidation?

Defaulted loans may be consolidated in certain circumstances. For example, if the borrower rehabilitates the loan by making satisfactory repayment arrangements through his/her loan servicer, he/she may be eligible to consolidate the loans. Also, borrowers may rehabilitate defaulted loans by consolidating them and agreeing to repay them in the income-based repayment plan.

What is the interest rate?

The interest rate on a federal consolidation loan is a fixed rate equal to the weighted average of the interest rates on the federal education loans that are being consolidated, rounded up to the nearest one-eighth of one percent.

For example, suppose a borrower has a $7,500 loan at 3.4% and a $10,000 loan at 3.86%, the interest rate on the federal consolidation loan would be rounded up to the nearest one-eighth of a point, or 3.75%.

Since July 1, 2013, the interest rate on new federal consolidation loans is no longer capped. Previously, the interest rate would have been capped at 8.25%.

A consolidation calculator may be used to calculate the interest rate on a federal consolidation loan.

What types of loans may be consolidated?

The following types of loans may be consolidated, including loans made in the FFEL program and the Direct Loan program.

- Direct Loans – Subsidized and Unsubsidized

- Grad PLUS Loans

- Parent PLUS Loans

- Federal Consolidation Loans

- Perkins Loans

- HEAL/HPSL Student Loans

- Nursing School Loans

What about private loan consolidation?

Private student loans may not be included in a federal consolidation loan.

Instead, several lenders offer private consolidation loans for consolidating or refinancing private student loans. The new private consolidation loan pays off the balances on the private student loans.

The private consolidation loan has a new interest rate based on the borrower’s (and cosigner’s) current credit history. This interest rate may be higher or lower than the weighted average of the current interest rates on the borrower’s private student loans. If the credit scores have improved significantly, this may lead to a lower interest rate, potentially saving the borrower money.

If a borrower’s private student loans were obtained with a cosigner, and the private consolidation loan does not involve a cosigner, consolidating the private student loans releases the cosigner from his/her obligation. This is effectively a form of cosigner release. However, since the interest rates on a private student loan usually depend on the higher of the borrower’s and cosigner’s credit scores, this may lead to an increase in the interest rate on the private consolidation loan, unless the borrower’s current credit score is better than the cosigner’s previous credit score.

While one could use a private consolidation loan to refinance federal education loans, this is generally not recommended. Usually the federal education loans have lower fixed interest rates, so a private consolidation loan may cost the borrower more. Also, federal student loans have numerous benefits and protections that are not available on most private student loans, such as generous deferments and forbearances, income-based repayment and public service loan forgiveness provisions. Federal education loans also offer death and disability discharges; only a handful of private student loan programs offer similar discharge options.

What about credit card consolidation, car loans, etc.?

Other forms of consumer credit, such as credit card debt, mortgages and auto loans, may not be included in a federal consolidation loan.

What about consolidating with my spouse?

Only one borrower’s loans may be included in a federal consolidation loan. Married borrowers may not consolidate their loans together, nor may a student’s Direct Loans be consolidated with the parent’s Parent PLUS Loan. (A parent who has a Parent PLUS Loan borrowed to pay for a child’s education and a Direct Loan borrowed to pay for the parent’s education may consolidate those loans together.)

Previously, married borrowers could consolidate their loans together. The Higher Education Reconciliation Act of 2005 repealed this provision, effective July 1, 2006, because of problems that occurred when the married borrowers subsequently got divorced. There was no way to unravel the joint consolidation, so the joint consolidation loans became a tie that binds beyond divorce.

I consolidated in the past, can I do it again?

Borrowers with an existing federal consolidation loan may consolidate again in a few circumstances:

- The borrower has at least one other FFEL or Direct Loan that will be included in the new consolidation loan.

- The borrower has one or more loans that have been submitted to a guaranty agency for default aversion and the borrower is seeking income-based repayment or income-contingent repayment.

- The borrower wishes to participate in public service loan forgiveness.

- The borrower is an active duty member of the U.S. Armed Forces and seeks to benefit from the “no accrual of interest” provision for loans made on or after October 1, 2008.

Note that reconsolidating a federal consolidation loan does not relock the interest rate.

How is the consolidation loan repaid?

The first payment on a federal consolidation loan is due no more than 60 days from the date of disbursement. Borrowers may get a 0.25% interest rate reduction by repaying the loans through auto-debit.

What repayment plan options are available on a federal consolidation loan?

The borrower may choose from several repayment plan options, including:

- Standard Repayment involves level monthly payments over a 10-year term

- Extended Repayment involves level monthly payments over a longer repayment term

- Graduated Repayment involves payments that start low but which gradually increase every two years

- Income-Based Repayment, Income-Contingent Repayment and Pay-as-You-Earn Repayment base the payments on a percentage of the borrower’s discretionary income

- Income-Sensitive Repayment is available for loans in the FFEL program and involves payment amounts that are based upon a percentage of annual income

There are two versions of extended repayment.

- If the borrower has $30,000 or more with a single lender, the repayment term is 25 years (this does not require consolidation)

- Otherwise the repayment term depends on the amount owed, with a 12-year term for $7,500 to $9,999 in debt, a 15-year term for $10,000 to $19,999 in debt, a 20-year term for $20,000 to $39,999 in debt, a 25-year term for $40,000 to $59,999 in debt and a 30-year term for $60,000 or more in debt

The various repayment plans based on income have different eligibility requirements and have different formulas for calculating the monthly payment.

- Income-Contingent Repayment (ICR) has a loan payment that is based on 20% of discretionary income, which is defined as the amount by which adjusted gross income exceeds 100% of the poverty line. The borrower’s loans must be in the Direct Loan program.

- Income-Based Repayment (IBR) has a loan payment that is based on 15% of discretionary income, which is defined as the amount by which adjusted gross income exceeds 150% of the poverty line. IBR is available to all borrowers, including borrowers with loans in the FFEL and Direct Loan programs.

- Pay-As-You-Earn Repayment (PAYE) has a loan payment that is based on 10% of discretionary income, which is defined as the amount by which adjusted gross income exceeds 150% of the poverty line. PAYE requires the loans to be in the Direct Loan program. At least one loan must have been made since 10/1/2011. The borrower must have been a new borrower as of 10/1/2007 with no loans made prior to that date.

- Revised Pay-As-You-Earn Repayment (REPAYE) also has a loan payment that is based on 10% of discretionary income, which is defined as the amount by which adjusted gross income exceeds 150% of the poverty line. There is no income requirement to qualify.

Of these, REPAYE and PAYE have the lowest monthly payments, followed by IBR. ICR has the highest monthly loan payments.

Are there any fees to consolidate?

No, there are no fees to consolidate federal student and parent loans, including the Direct Loan and Federal PLUS loan. However, if a borrower was receiving a loan discount or “borrower benefit” from a FFEL program lender, the borrower may lose that benefit upon consolidation since the discounts are not provided by the promissory note.

Is there a credit check required to consolidate?

No, no credit check is required to consolidate federal student loans.

Are there any early payment/repayment fees or penalties?

No, there are no early repayment penalties for a federal consolidation loan. To make extra payments, the borrower may specify “Extra payment to principal” on any prepayment.

Borrowers who are planning on making extra payments on their loans may wish to avoid consolidation. When a borrower’s loans are kept separate, the borrower can target the loans with the highest interest rates for accelerated repayment, saving money. Consolidation replaces these loans with a single loan with a single interest rate, eliminating the possibility of prepaying specific loans.

How do I apply for a federal consolidation loan?

The federal Direct Consolidation Loan application can be completed online at the U.S. Department of Education’s web site, StudentLoans.gov.

Do I continue making loan payments while my consolidation application is in process?

Yes! Borrowers should continue making payments on their existing loans until they are notified that the loans have been paid off through the consolidation process. Consolidation can take anywhere from 30 to 90 days. It’s important that borrowers don’t fall behind on their payments. Once the consolidation is complete, the servicer will send the borrower a new repayment schedule, with the new monthly payment amount, due date, and payment address.

How long does a consolidation take?

Consolidation can take anywhere from 30 to 90 days; in rare cases, it may take longer. The process involves the transmission and processing of payoff statements, called Loan Verification Certificates (LVCs), which can take time.

What do I do if I am not eligible to consolidate?

Some borrowers are not eligible to consolidate their federal student loans because of a previous consolidation loan, but are locked into a high interest rate from several years ago. There are a few options for a lower interest rate for these borrowers. The main drawback is these involve refinancing into something other than a federal consolidation loan, causing the borrower to lose the benefits of a federal student loan. These include:

- Obtaining a home equity loan or line of credit to pay off the loan.

- Obtaining a personal line of credit from a bank or credit union.

- Considering a private consolidation loan.

Even if the borrower has bad credit because of a previous loan default, his/her parents may be able to obtain one of these forms of financing at a low interest rate, making it easier for the borrower to repay his or her student loans.

Can I get a deferment or forbearance?

Yes! Borrowers who obtain a federal consolidation loan retain all of the benefits of a federal student loan, including:

- Deferment of the loan payments while the borrower is enrolled in school on at least a half-time basis. This includes borrowers who graduated but are returning to school for further education.

- Economic hardship deferment for up to 36 months.

- Forbearance for up to 36 months.

- Full or partial loan forgiveness through various federal loan forgiveness programs, such as public service loan forgiveness and teacher loan forgiveness.

To obtain a deferment or forbearance, contact the servicer after the loan has been consolidated to request a deferment or forbearance form.

Did you know that consolidation may reset the clock on deferments and forbearances? It’s true! Borrowers who have already reached the time limit on their forbearances and deferments may reset the clock to zero by consolidating. A consolidation is a new loan, eligible for the same deferments and forbearances as the original federal student loans.

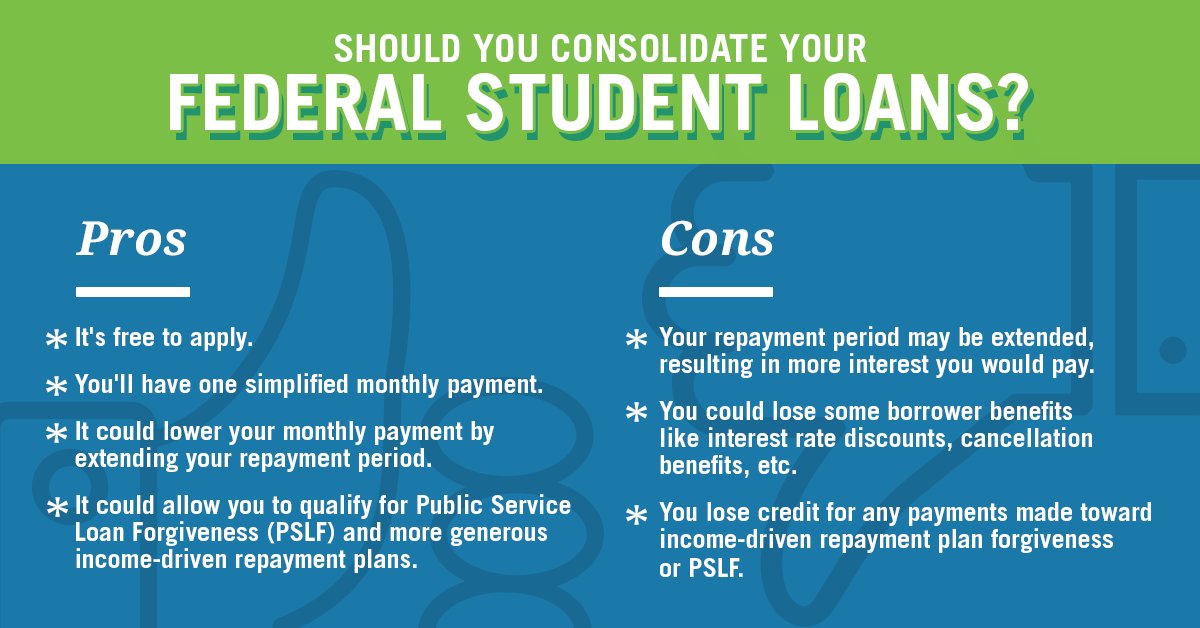

Why Consolidate?

Consolidating helps borrowers manage multiple loans by replacing them with a single loan. Borrowers can also reduce the burden of federal student loan payments on their monthly budget by choosing a repayment plan with a lower monthly payment.

Why Not Consolidate?

There are, however, some reasons why borrowers might not want to consolidate their loans.

- Reducing the monthly payment often involves extending the repayment term on the loan. This will increase the total interest paid over the life of the loan. For example, while increasing the repayment term from 10 years to 20 years may reduce the monthly payment by a third, it more than doubles the total interest paid.

- Borrowers who consolidate their federal student loans during the grace period lose the remainder of the grace period.

- Borrowers who consolidate Perkins Loans lose the subsidized interest benefit on the Perkins Loan, as well as the favorable loan forgiveness options.

- When borrowers with accrued but unpaid interest consolidate their loans, the interest gets capitalized (added to the loan balance). This causes interest to start being charged on the interest, increasing the cost of the loan.

- Borrowers do not necessarily need to consolidate to get extended repayment or income-based repayment.

Repayment Guidelines

Depending on the total amount of your consolidation loan, the government has set the following repayment periods:

| Loan Balance | Repayment Period |

|---|---|

| Less than $7,500 | 10 years |

| $7,500 to $9,999 | 12 years |

| $10,000 to $19,999 | 15 years |

| $20,000 to $39,999 | 20 years |

| $40,000 to $59,999 | 25 years |

| $60,000 and above | 30 years |